THE COMPLETE PICTURE

>> Four indicators across three time frames.

>> When all the Sherman Portfolios indicators are positive status, we read the market as being in a Bull Market.

1. DELTA-V — Positive since June 27, 2025

2. GALACTIC SHIELD — Positive since April 1, 2023

3. STARFLUX — Positive since May 12, 2025

4. STARPATH — Positive since August 15, 2025

The shorter term picture:

>> GALACTIC SHIELD — POSITIVE, This indicator is based on the combination of U.S. and International Equities trend statuses at the start of each quarter.

>> STARFLUX — POSITIVE, Starflux ended the week 5.28 (down 24.68% last week). This short-term indicator measures U.S. Equities. It measures the trend-strength of the Russell 3000 index.

>> STARPATH — POSITIVE, This indicator measures the interplay on dual timeframes of our Type 1s + the Russell 3000 + our four most ‘pro-cyclical’ Type 3s, vs. Cash

The big picture:

The ‘big picture’ is the (typically) years-long timeframe, the same timeframe in which Cyclical Bulls and Bears operate.

>> The Sherman Portfolios DELTA-V Indicator measuring the Bull/Bear cycle finished the week in a Bull status at 70.98, down 3.01% from the prior week’s 73.18. It has signaled Bull since June 27, 2025.

>> The Sherman Portfolios DELTA-V Bond Indicator measuring the Bull/Bear cycle finished the week in BULL status at 64.75, down 4.19% from the prior week’s 67.58. It has signaled Bull since December 15, 2023.

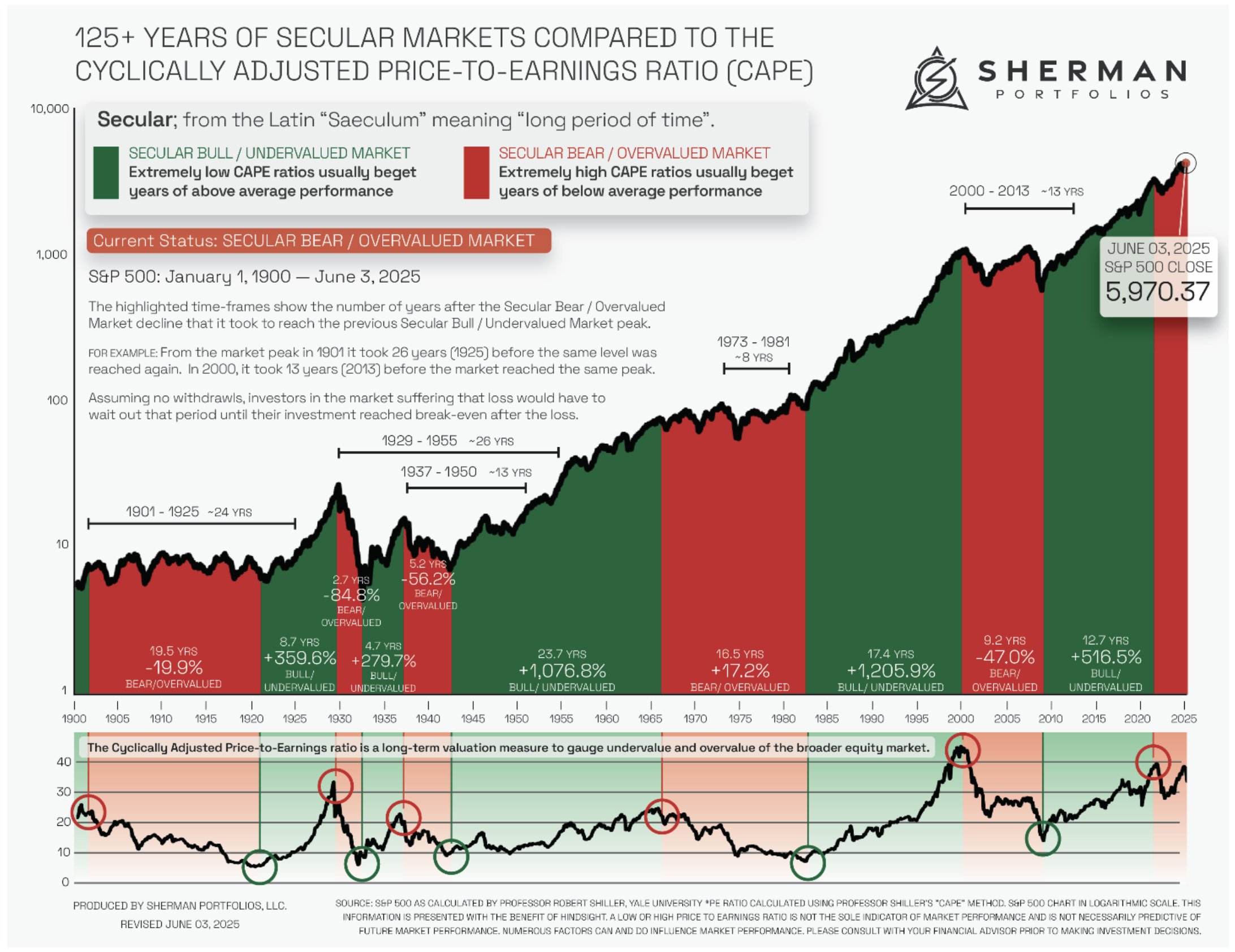

The very big picture (a historical perspective): The CAPE is now at 39.67.

The cyclically adjusted price-to-earnings ratio (CAPE) can be used to smooth out the shorter-term earnings swings to get a longer-term assessment of market valuation. An extremely high CAPE ratio means that a company’s stock price is substantially higher than the company’s earnings would indicate and, therefore, overvalued. It is generally expected that the market will eventually correct the company’s stock price by pushing it down to its true value.

In the past, the CAPE ratio has proved its importance in identifying potential bubbles and market crashes. The historical average of the ratio for the S&P 500 Index is between 15-16, while the highest levels of the ratio have exceeded 30. The record-high levels occurred three times in the history of the U.S. financial markets. The first was in 1929 before the Wall Street crash that signaled the start of the Great Depression. The second was in the late 1990s before the Dotcom Crash, and the third came in 2007 before the 2007-2008 Financial Crisis. https://www.multpl.com/shiller-pe

Note: We do not use CAPE as an official input into our methods. However, we think history serves as a guide and that it’s good to know where we are on the historic continuum.

Note: We do not use CAPE as an official input into our methods. However, we think history serves as a guide and that it’s good to know where we are on the historic continuum.

THIS WEEK IN THE MARKETS

U.S. Markets:

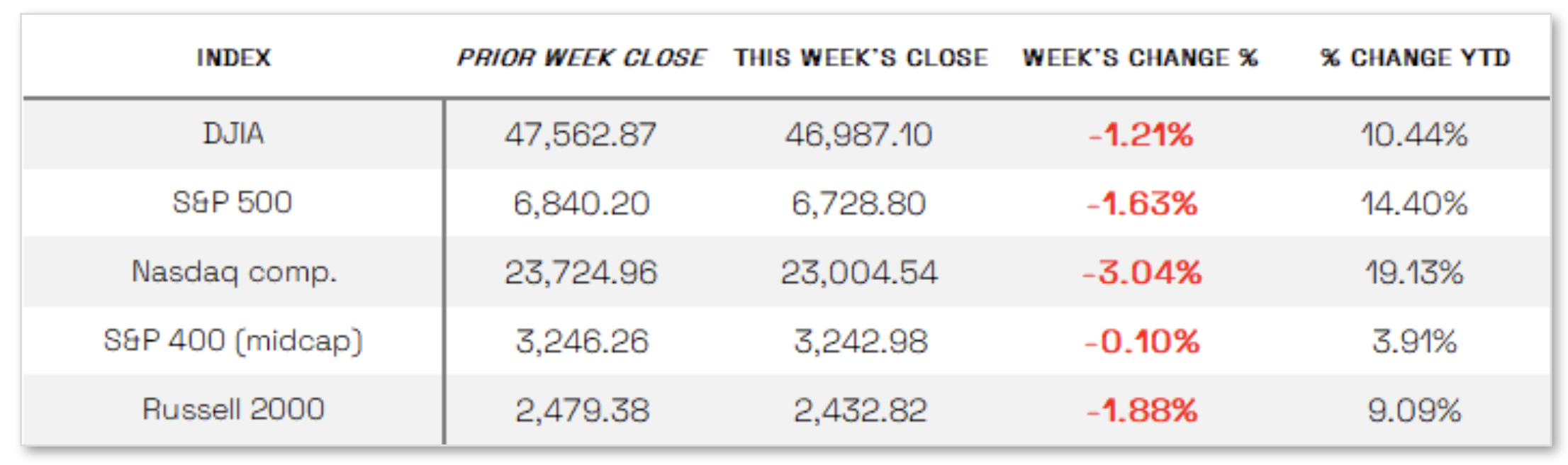

Tech drags indexes lower: U.S. stocks ended their three-week winning streak as a sell-off in technology shares dragged major indexes lower, with concerns over high valuations and increased scrutiny of artificial intelligence (AI) spending weighing on growth-oriented names that had fueled gains since early April. The Nasdaq Composite led declines, and the Russell 1000 Growth Index lagged its value counterpart by 288 basis points—the widest gap since February. Broader sentiment was further dampened by the ongoing U.S. government shutdown, which became the longest on record and raised worries about its economic impact. Headlines intensified after the Federal Aviation Administration ordered airlines to cut flight schedules due to staffing shortages, while investors grew increasingly concerned about missing government data and potential effects on GDP growth.

Looking at the US Indexes:

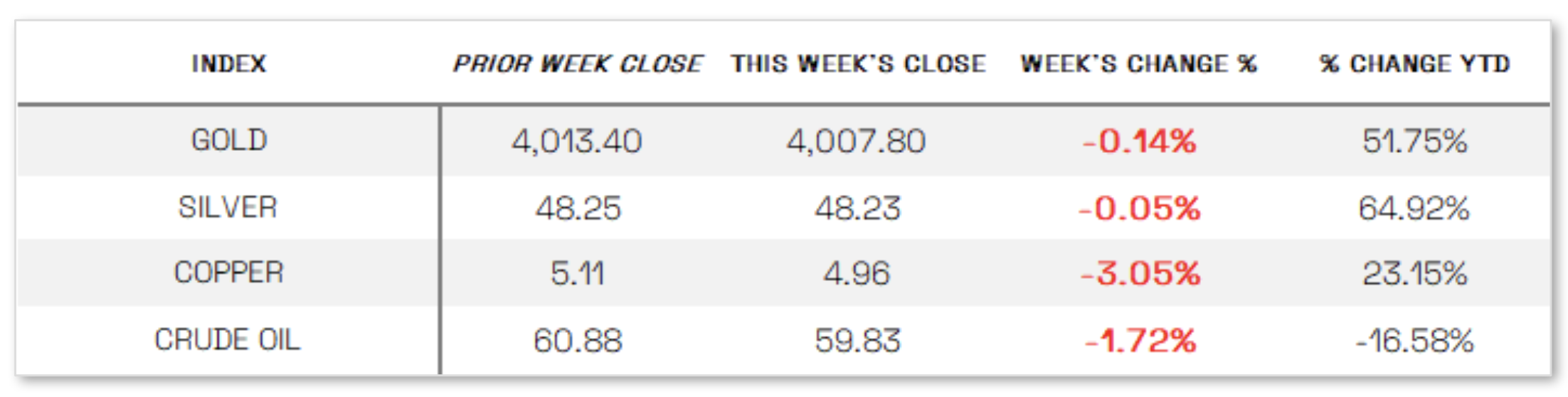

U.S. Commodities/Futures:

THE VOLATILITY INDEX (VIX) closed at 19.08 this week, a 9.4% increase vs last week’s close of 17.44.

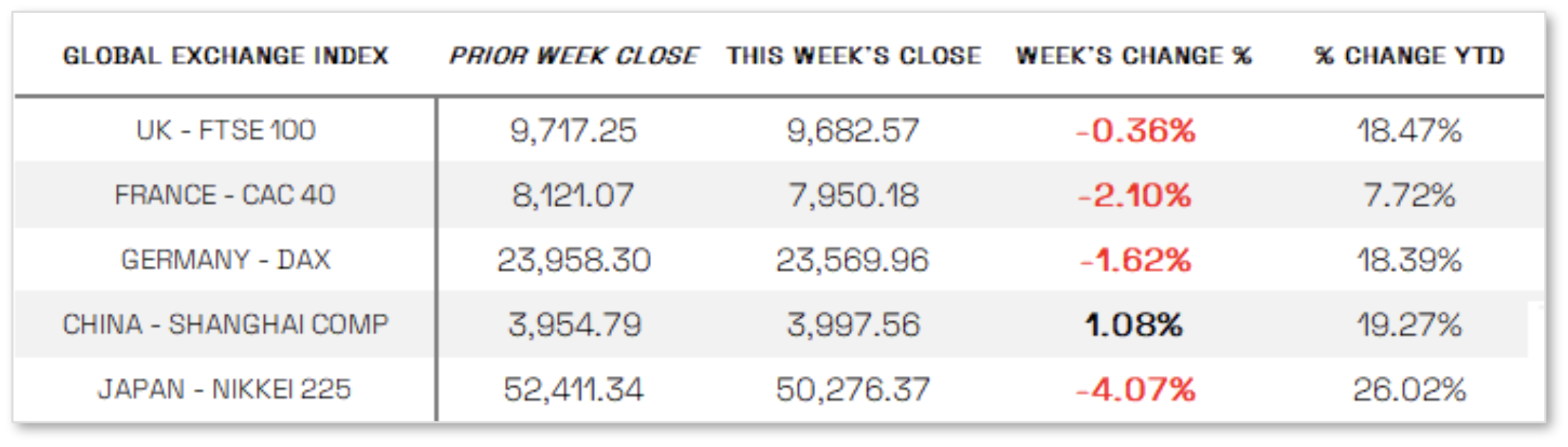

International Markets:

THIS WEEK’S ECONOMIC NEWS

U.S. Economic News:

Economic outlook mixed:

With the government shutdown limiting official data releases, investors turned to private-sector reports for insight into the labor market and economic activity. ADP’s October report showed private employers added 42,000 jobs, marking a rebound after two months of declines, though gains were uneven as sectors such as professional services, information, and leisure and hospitality continued to shed jobs for the third straight month, and pay growth remained flat. Separately, Challenger, Gray & Christmas reported that employers have cut nearly 1.1 million jobs so far this year—a 65% increase from the same period last year—with October’s 153,074 layoffs marking the highest monthly total since 2003. On a more positive note, the Institute for Supply Management indicated that services activity returned to growth in October, as its Services PMI rose to 52.4% from 50.0% in September, driven by stronger new orders, while manufacturing contracted for the eighth consecutive month.

International Economic News:

EUROPE: In local currency terms, the pan-European STOXX Europe 600 Index fell 1.24% as concerns over overvaluation in artificial intelligence-related stocks weighed on sentiment, leading to broad declines across major markets: Italy’s FTSE MIB slipped 0.60%, Germany’s DAX dropped 1.62%, France’s CAC 40 lost 2.10%, and the UK’s FTSE 100 declined 0.36%. The Bank of England (BoE) kept its key interest rate unchanged at 4.0%, with a narrow five-to-four vote, while Governor Andrew Bailey’s comments supported expectations for a potential rate cut in December, noting that current market projections of a 3.5% terminal rate within three years reflected a “sensible path.” Elsewhere, Sweden’s Riksbank maintained its policy rate at 1.75%, signaling it would likely stay there “for some time,” and Norway’s Norges Bank also held steady at 4.0%, with Governor Ida Wolden Bache emphasizing that high inflation means it will take time before rate reductions are appropriate.

JAPAN: Japan’s stock markets retreated over the week, with the Nikkei 225 dropping 4.07% and the broader TOPIX Index falling 0.99%, following record highs in late October. After strong gains driven by AI-related technology and major chip companies, investors grew cautious about stretched valuations and moved to take profits. Broader concerns over inflated AI valuations dampened risk appetite, prompting a flight to safety that strengthened the yen to the mid-JPY 153 range against the U.S. dollar, aided by Finance Minister Satsuki Katayama’s comments reaffirming the government’s vigilance over rapid currency movements. Meanwhile, the 10-year Japanese government bond yield edged up to 1.68% from 1.65% amid expectations of further monetary tightening by the Bank of Japan (BoJ), which continues to watch wage trends closely as a guide for future rate decisions. Nominal wages rose 1.9% year over year in September, up from 1.5% in August, but real wages declined for the ninth straight month—down 1.4%—as inflation continued to erode income gains.

CHINA: Mainland Chinese stocks rose modestly for the week as easing U.S.-China trade tensions lifted investor sentiment, with the CSI 300 Index gaining 0.82% and the Shanghai Composite Index up 1.08%, while Hong Kong’s Hang Seng Index advanced 1.29%. The CSI 300’s latest increase brought it to its highest level in nearly four years, even amid ongoing concerns about China’s economic outlook. Optimism was fueled by a one-year trade truce reached between the U.S. and China following the presidents’ meeting at the Asia-Pacific Economic Cooperation (APEC) summit in South Korea. Although the summit produced few concrete outcomes, analysts at T. Rowe Price Associates noted that the prevailing tone reflected growing pragmatism among participating nations—seeking to trade where possible and hedge where necessary in an increasingly complex global landscape. Still, they cautioned that long-term strategic competition between the U.S. and China remains a defining feature that will likely extend beyond trade.

Sources:

>> All index and returns data from Norgate Data and Commodity Systems Incorporated and Wall Street Journal.

>> News from Reuters, Barron’s, Wall St. Journal, Bloomberg.com, ft.com, guggenheimpartners.com, zerohedge.com, ritholtz.com, markit.com, financialpost.com, Eurostat, Statistics Canada, Yahoo! Finance, stocksandnews.com, marketwatch.com, visualcapitalist.com, wantchinatimes.com, BBC, 361capital.com, pensionpartners.com, cnbc.com, FactSet, Morningstar/Ibbotson Associates, Corporate Finance Institute.

>> Commentary from T Rowe Price Global markets weekly update — https://www.troweprice.com/personal-investing/resources/insights/global-markets-weekly-update.html

Disclosures: This material and any mention of specific investments is provided for informational purposes only and is not intended to be investment advice or a recommendation to take any action. The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. The market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. Past performance does not guarantee future results.